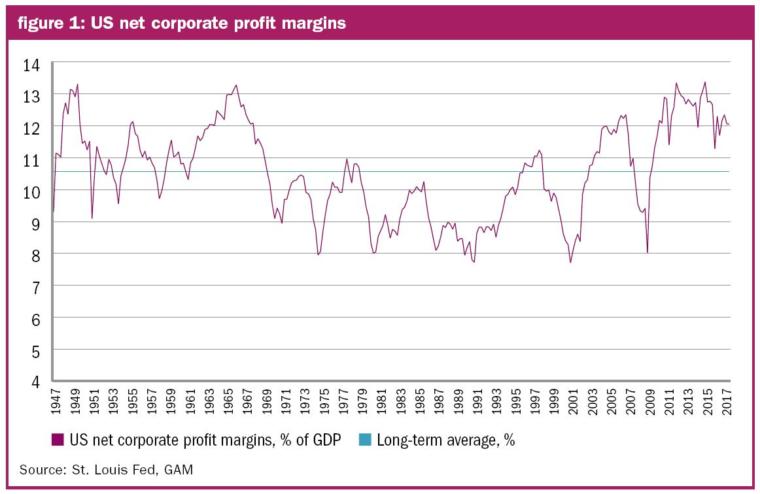

US profit margins as a percentage of GDP are close to all-time highs. For many, this is a sign of corporate health further corroborated by the S&P 500’s second quarter profit growth of over 10 per cent on the previous year. Good news it would seem, but the question for investors is how long will it last and are sustained high profits even desirable?

Jeremy Grantham described profit margins as a proportion of GDP as “one of the most mean-reverting measures available. If profits stay high, then there is something wrong with the system.” This statement goes to the heart of the free market and speaks to Schumpeter’s creative destruction theory. In a healthy, well-functioning capitalist system, high profitability should be temporary as new entrants nibble at corporate incumbents and eventually steal their share through the innovation of superior products and services. Conversely, much praise is now being directed at large-cap listed technology stocks such as Facebook and Amazon who use their cash piles and the network effects of their huge user bases to dust off the competition. The key issue is whether this is a fundamentally good thing.

For some investors, the new paradigm (remember that?) justifies structurally higher equity allocations. But memories could prove to be painfully short because competition is never far away, even when it appears to have been vanquished. In emerging markets, a new cadre of companies with huge scale in their domestic markets are starting to expand. Past examples include the rise of Hyundai cars in Europe, but more pertinent to today’s higher-profits debate are the new digital platforms such as Alibaba. These firms are like Trojan horses in that they permit small and medium-sized companies to gain a foothold in mature markets, allowing them to challenge larger firms without requiring their own logistical and marketing functions. They in turn could then list and inject fresh competition into the stock markets.

Permanently higher? Or ripe for competitive destruction?

Asking for volatility?

To wish for a shake-up in the agents of profit generation feels a lot like asking for market volatility. But in the long term, institutionalising the sources of corporate profits among a small handful of firms is not desirable. Most obviously, it makes for poor diversification and worse market consequences when regime change does come about. It can drive entire markets upwards, and potentially downwards too. This has certainly been the case as the large cap listed US technology stocks have been a significant contributor to the S&P 500’s progress in 2017. Between them, Facebook, Microsoft, Apple, Google and Amazon are now worth around $3tn. And such situations can create negative feedback loops.

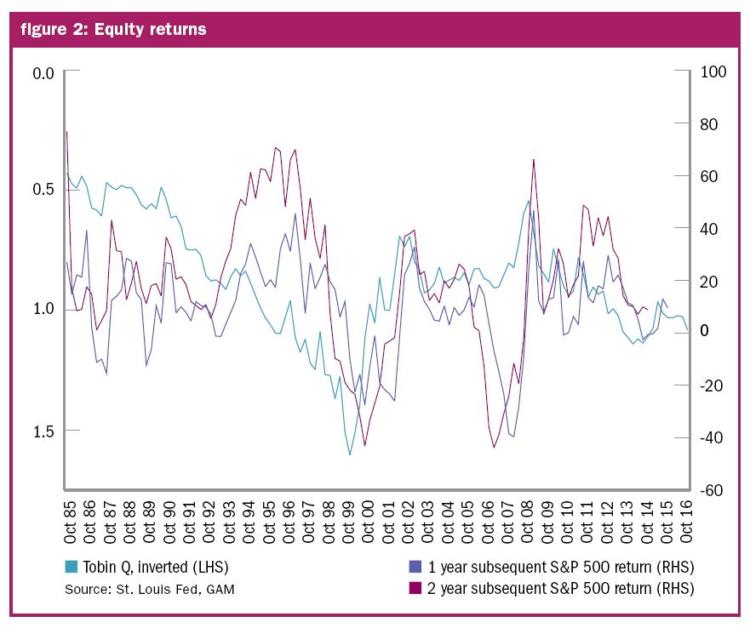

The issue is compounded by the fact that at the market level, the US is now richly valued. Whether valuation measures like the Shiller CAPE, market cap/gross value added (a tax adjusted form of GDP) or the Tobin Q are used, the implication, based on long term history, is that future equity market returns will be subdued from here onwards. Just days before the tumultuous market events of 1929, US economist Irving Fisher triumphantly declared that stock prices were on a “permanently high plateau”. A change in today’s profit landscape might inflict pain but it would also serve to rebalance the equity market and, for those investors sitting on the sidelines, any such development could be an opportunity to buy into the market at attractive levels.

Figure 2 illustrates that high valuations suggest lower equity returns from here.

This time will not be different

Monopolistic situations are intrinsically unhealthy for markets in the long run but historically they have tended to adjust, sometimes spectacularly. There is no reason to believe that this time will be any different, particularly given trends in developing economies which are producing new sources of head-on competition. This is to be welcomed, rather than feared.

As pioneering antitrust legislator John Sherman said in 1890: “If we will not endure a king as a political power, we should not endure a king over the production, transportation and sale of any of the necessaries of life.” Investors today are citing market inefficiencies to rationalise super-elevated profits and high returns into the future. But it is right and desirable that such a situation should eventually be challenged by new competitive and disruptive forces. An active and thematic approach to investment management will be key to navigating such changes successfully.

Julian Howard is head of multi asset solutions at GAM

Charity Finance wishes to thank GAM for its support with this article