Having a bespoke portfolio tailored to specific investment goals is often considered solely the preserve of private clients. With the fiduciary responsibilities placed on charity trustees, however, it may be sensible to opt for a more personalised, bespoke investment solution, by developing a relationship with the investment manager.

For charities that are fortunate enough to have excess capital to invest, their trustees have to consider and adhere to a set of considerations and legal requirements when investing their charity’s assets for a financial return. While the Charity Commission has published Charities and Investment Matters: a Guide for Trustees, also known as CC14, investment still remains a complex area for many, especially for those who are not experienced investors.

In general terms, charities can invest in a wide range of assets, including cash deposits and shares, as well as bonds issued by both governments and companies. Collective investment schemes (pooled funds), commodities, derivatives and buildings or land are also approved charitable investments. Furthermore, trustees are responsible for ensuring that strategic decisions about a charity’s assets are in line with its overall objectives and they can decide to make investment decisions themselves, if they have the necessary skills and experience. However, most trustees choose to delegate the decisions to a professional investment manager.

Having identified capital for investment, the key decision then is what assets to hold, as asset choice is the primary driver of long-term returns. How these assets are held however (directly or in pooled funds) and who you should entrust them too, should be a secondary consideration.

For charities with smaller amounts of capital to invest, adopting a pooled fund approach, rather than having a bespoke directly invested portfolio, has for some time now been the go-to option. Using a common investment fund (CIF) or a Charity Authorised Investment Fund (CAIF), ensures that these types of charities have access to a wide range of securities, which might be difficult to achieve as part of a directly invested portfolio, in a cost effective manner, given the portfolio size. Furthermore, the administrative ease with only one main fund holding, accounting and record keeping is kept simple for the charity. Many of these pooled vehicles are also dual-regulated by the Charity Commission and the Financial Conduct Authority (FCA), offering trustees additional comfort.

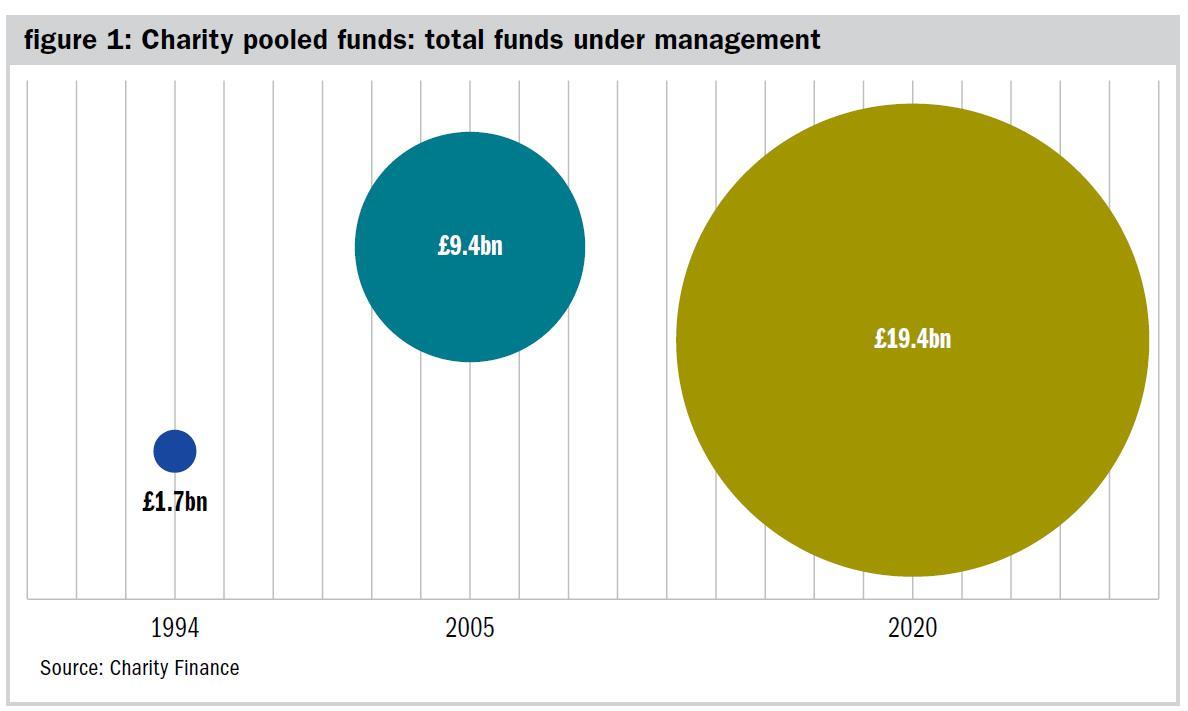

Pooled funds established for charities have been around for over 50 years but as figure 1 shows, the market has grown significantly since 1994. There are currently 65 investment funds exclusive to, or aimed at, charities, with invested capital of almost £20bn. Both the number of funds and assets invested has grown steadily over the last 25 years; furthermore, new funds continue to be launched. All these funds are invested in a slightly different way, with different risk profiles and investment objectives, with some are aimed at specific charitable organisations. While there is no doubt this method of accessing markets is appropriate for some, we believe that accessing financial markets is only one part of a complex equation. By investing this way you adopt a standardised approach with little flexibility to adapt to changing circumstances. We believe charities now demand more from their investment manager rather than just investment advice.

Historically, many charities have felt that a bespoke portfolio is not an option for them, given the size of the assets they want to invest. However, the landscape has changed over the last two decades as trustees have had to embrace new regulation, consider environmental, social and governance (ESG) requirements that continue to develop and evolve, look at new asset classes, whilst the opportunity set for investment has grown exponentially. There is a lot more choice now and arguably the amount of information that is available instantly, makes it ever more important to implement a dynamic asset allocation strategy.

While investing in a CIF or a CAIF might be a cost effective solution for some, we have always advocated that a bespoke portfolio is available to charities, regardless of the size of capital that they want to invest, given the option of a flat charging structure, such as we adopt. We are often asked why we advocate investing in a bespoke manner rather than pooling funds and we feel that the advantages are clear:

1. Flexibility

With a bespoke portfolio, attitudes to risk, ESG requirements, and investment objectives can change over time, depending on specific requirements. With a bespoke portfolio you are able to adjust and adapt quickly and efficiently, taking advantage of changes in market sentiment, while also ensuring that the investments fully reflect the charity’s short and long-term goals and aspirations. While there is a high commonality of investments held across charity portfolios, they can be treated individually, as many have special instructions and/or investment restrictions.

2. Highly personable

The relationship between a charity and investment manager works best when trustees have a good understanding of the investment process and we spend a lot of time with trustees, educating them if needed, on different asset classes and financial markets. Furthermore, drawing on our experiences with developing private client relationships, we dedicate a lot of time to communicating with trustees, ensuring that we understand the intricacies of their charity. We feel this promotes much better outcomes for both.

3. Communication

Bespoke portfolios, on the whole, ensure that the investment manager/relationship manager role is combined and therefore nothing is lost in translation. This promotes a better understanding of a charity’s aspirations and objectives and again promotes accountability and better client outcomes. The trustees have a direct line of communication into the team who are managing and investing the charity’s assets, ensuring the portfolio not only reflects the charity’s overarching investment objective, but also its goals and values.

4. Cost-effective

Charging structures have changed over the years with more of a focus now on all in fixed percentage management fees. With no dealing costs, this ensures that charities with small amounts of capital to invest can avoid paying high charges when dealing in smaller amounts.

Our experience highlights that smaller charities are often surprised to hear that they can have a bespoke portfolio. They soon realise that the additional services that come with having a personalised service, the increased flexibility and the direct communication that they have with those managing their assets, can becomes invaluable.

Given the changing landscape and the growing number of requirements charities need to adhere to from a regulatory perspective, we find that trustees feel more comfortable investing in a portfolio built around their specific needs, with an experienced team which has the tools at its disposal to deliver this. Furthermore, being able to talk to the team that manages the money can lead to better outcomes while ensuring that their investment objectives and aspirations are met.

Sam Barty-King is an investment director at JM Finn

Charity Finance wishes to thank JM Finn for its support with this article