The last year has been an extraordinary period in world history, with many of the issues that have dominated 2020 likely to dominate 2021 as well. Financial markets are of course no different and 2021 looks set to be another challenging year for investors; we enter the next stage of Covid-19 as a vaccine emerges but the full fallout of the pandemic remains to be seen, governments across the world look set to continue large scale fiscal spending and geopolitical tensions looks set to continue. These issues may present considerable challenges to many charitable portfolios.

The most common approach to handle matters like this in the past has been to hold a balanced portfolio often called the “60/40”, which relates to the holdings in equities (60%) and bonds (40%). However, we believe that this portfolio structure, the bedrock of charitable investment over the past 50 years, may not be as resilient going forward in 2021 and beyond.

We will explore why this strategy has worked, why it may be vulnerable now, and why, in the years ahead, charity investors may need something different.

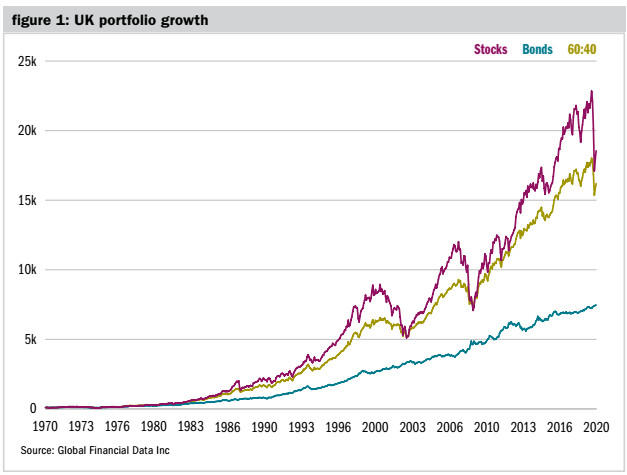

Before we look forward, it is important for us to first look back. The 60/40 portfolio has served investors well for the past 50 years. It has been the allocation of choice for traditional balanced portfolios: 60% in equities for the good times, 40% in bonds for the bad (and for the yield – especially important for charities and in particular those that are permanently endowed).

Equities have performed best. A buy-and-hold strategy has worked perfectly for investors who haven’t needed to draw on their portfolios. In times of market stress, bonds have dampened portfolio volatility. Having 40% of the portfolio in bonds helped investors during the dot.com bust and the global financial crisis.

However, most investors need to draw cash from their portfolios at some point, which means that volatility or standard deviation becomes relevant – particularly over shorter time periods. The standard deviation of a portfolio comprised solely of equities was significantly higher than the standard deviation of a 60/40 portfolio, but only improved the annualised return by 0.8%. In other words, the 60/40 portfolio has achieved better risk-adjusted returns.

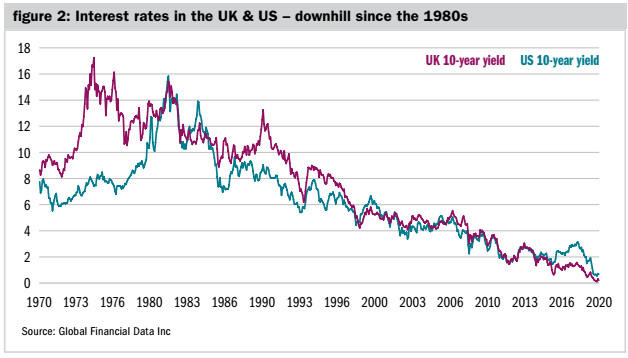

So, why has this combination of bonds and equities been so powerful for investors? Well, since the late 1970’s several disinflationary forces have prevailed. Ageing demographics, the growth of IT, the re-emergence of China and globalisation amongst others. These forces have kept a lid on inflation and allowed central banks to operate without worrying too much about rising inflation. As a result, central banks across the world have been able to lower interest rates, steadily but consistently. As rates and yields have fallen, bond prices have risen, and so has the price of equities. Both bond and equity markets have had a 40-year tailwind of falling interest rates, meaning holding both has been a great decision. However, at current levels interest rates can’t fall much further from here – so what does the future hold for bonds?

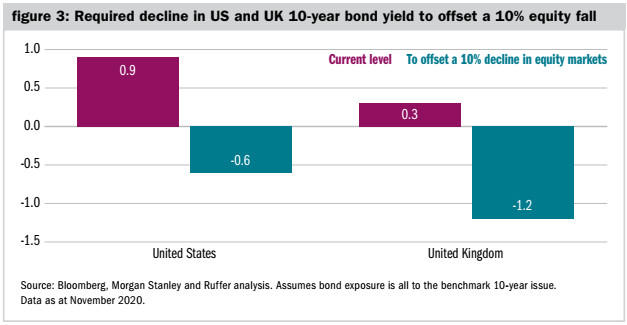

Bonds have historically acted as an offset to equities in market crises. In times of market panics, central banks cut interest rates, which push up the prices of bonds. This helps to offset damage done in the 60/40 portfolio by the holdings in equities, which are likely to suffer in times of economic stress, such as in 2008. So, protection is a key reason to hold normal conventional bonds in a portfolio.

But figure 3 demonstrates that bonds are very unlikely to do this job in the future. The blue bars illustrate how far yields must fall to offset a 10% decline in equity markets for a 60/40 portfolio.

With bond yields already so low, there is no scope for the multi-decade bull market in bonds to continue indefinitely. From this point there appears to be an asymmetric risk; bonds provide poor (in some cases negative) yields and limited downside protection. In addition, bonds also provide little to no income at all, making it harder for charities to derive the same level of income now that they received say 10 years ago, without having to take on an ever higher level of risk.

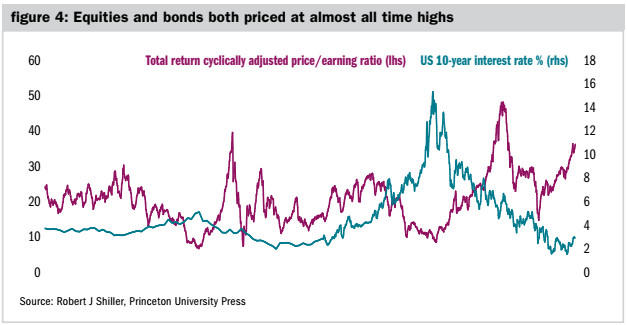

Looking forward, when forecasting future returns, a good rule of thumb to use (although it is by no means a guarantee) is to look at the price an investor pays for an asset. The higher the price, the more likely it is that the investor will receive below average returns in the future and vice versa.

When we look at the key components of the 60/40 portfolio it is clear that both bonds and equities trade at valuations close to all-time highs. Yes, if rates are low, then using a discounted cash flow to value stocks (estimating the present value of future earnings) goes some way to justifying record-high valuations. Yet by whichever metric you choose to use, equity valuations appear stretched and therefore pose a significant risk to investors.

And momentum within stock markets can change and change quickly, catching investors off guard and causing serious pain. For example in November 2020, when news of an effective vaccine caused 10-15% to be wiped off the value of several major tech stocks – the lockdown winners – in one day. And in that scenario bonds did little to protect portfolios.

Looking even further forward, the scale of fiscal policy set to be unleashed by governments, combined with record low interest rates we believe is a powerful cocktail that is likely to bring inflation back as a key risk to markets, something we as investors have not had to deal with for a number of decades.

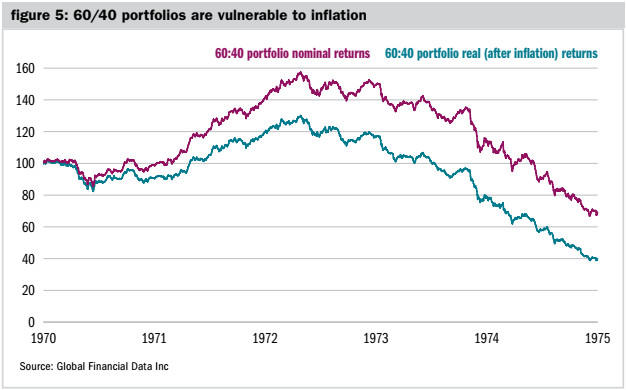

Looking at the last time inflation was a real threat reminds us just how damaging it can be. Nominal returns in the 1970s were reasonable, but when you factor in the high inflation, the picture changes. You lost 60% of the real value of a 60/40 portfolio between 1970 and 1975.

Most investors alive today have never encountered significant inflation. Quantitative easing boosted asset prices but had no impact on consumer prices. Investors do not believe that inflation is coming. However, the deflationary forces of the past five decades are waning and the response to the pandemic has seen a monumental rise in government spending.

Most central banks have used rhetoric suggesting they are willing to let inflation overshoot their targets. The inflationary chips are stacking up. Inflation is a menace worth protecting against. It is a major risk to the conventional 60/40 portfolio. Equities suffer, as the experience of the 1970s shows, but their earnings will eventually grow as prices rise. Inflation is a much bigger risk to bonds – they will not protect the real value of portfolios. Alternative assets are required. Inflation linked bonds, issued by governments that have their value tied to inflation, look to be a good asset to hold in such an environment. Conventional bonds, with fixed yields, do not.

The key to navigating these current issues will lie in diversifying beyond the traditional balanced portfolio, which we believe will suffer as the market transitions into this new investment regime from 2021 onwards. The potential for both bonds and equities to fall together in such an environment will be high and the damage this could do to charity portfolios is potentially severe. As a result, investors will need to seek assets and managers with low correlation to these markets, and negative correlation at points of stress.

Ajay Johal is an investment manager at Ruffer